Q1 Updates to profiled companies: Warsaw Stock exchange $GPW, Automatic Bank Services $SHVA, BayCurrent $6532, RS Technologies $3445 and Zengame $2660

If you're new here—welcome! Lots of new people are receiving this email for the first time.

A bit about me: I write about small, global stocks that I believe are high quality and trading at cheap valuations. I run a concentrated portfolio, and the goal is to outperform the U.S. indexes over the long term (I’m based in the U.S.).

Almost every company I write about is a stock I personally own. This isn’t an idea-generation newsletter with new picks every week, it’s a reflection of my filters and how I think about my own portfolio actions. That means there may be weeks (or longer) with no new ideas. When I do publish, it’s because I’ve done the work and put capital behind it.

I haven’t published any articles recently because I didn’t feel any of my new ideas were strong enough to add to the portfolio. Instead, I’ve taken this time to review the positions I’ve already profiled to see how they’ve progressed.

Here are the companies I’ve written about, with performance and updates since the initial write-up:

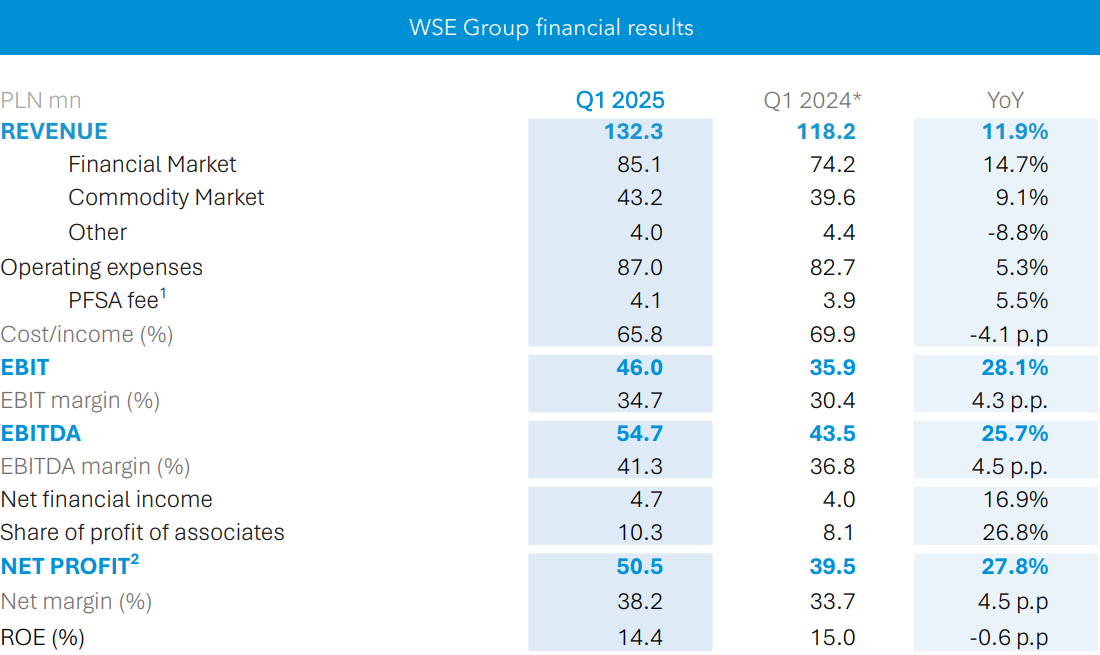

Warsaw Stock Exchange $GPW

Write-up date: Jan 18, 2025

Warsaw Stock exchange has been performing particularly well since I first wrote it up on 1/18/2025. The company released its Q1 numbers and turnover reached record highs. For most of GPW’s earnings, turnover is the main driver of performance as opposed to other major exchanges where an increasing portion of earnings is driven by clearing and data sales.

For a business like $GPW it is extremely important to pay attention to the revenue growth because the company has operating leverage. This means for every new dollar of revenue generated, they may earn $1.10 or 1.20 of Net Income because the fixed costs (servers, software infrastructure, and core engineering teams) are already paid for.

This is an extremely powerful principle when the company only trades for 13 times earnings and 12.2 EV/EBIT.

The next thing to watch for with $GPW is the transition from an exchange company to a software company, which over time has happened to nearly every major stock exchange after a certain scale. Take Nasdaq for instance, it began as a pure trading platform but has since evolved into a fintech and data company, with over 60% of its revenue now coming from recurring sources like software, analytics, and cloud-based infrastructure. This transformation unlocked higher multiples, greater predictability, and stronger margins — a path that $GPW may similarly follow if it can successfully shift from transactional revenue to SaaS-like, sticky software offerings.

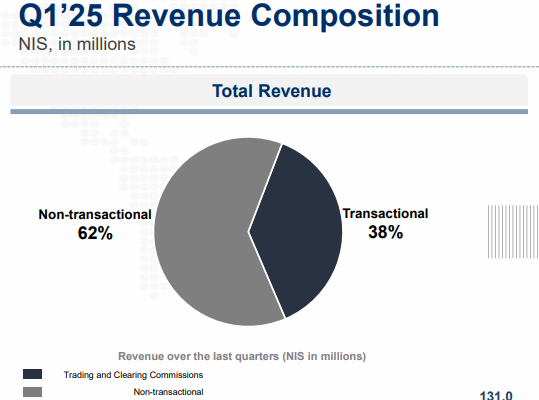

I also own the Tel Aviv Stock Exchange, that has done a better job than $GPW at doing this transformation, and the stock price has reflected this. My investment is up 185% from purchase on January of 2024.

Here is the Q1 2025 breakdown of $TASE’s revenue composition:

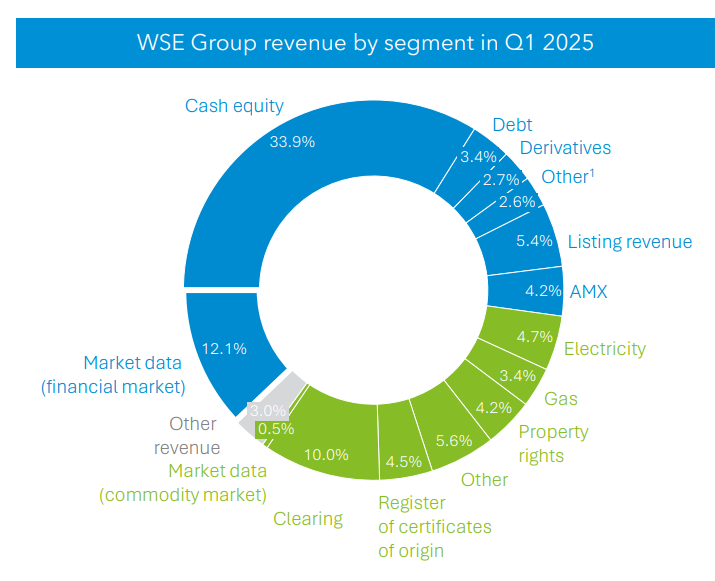

Compared with the Warsaw Stock exchange ( I would estimate 30% non transactional depending on how you classify)

Overall, you are still getting a great price for this security and there is plenty of growth to go.

RS Technologies $3445

Write up date: 4/25/2024

RS Technologies has also been an outperformer for my portfolio. This is mostly due to increased sentiment for the Japanese markets, as not much material news has come out about the company. The quick thesis is that the company is heavily discounted based on assets, and the assets are vital, some commoditized, Semiconductor products that have steady demand for the foreseeable future. They are likely the low cost producer in their main business, and their direct sales approach gives them an edge in all the other businesses.

Automatic Bank Services $SHVA

Write up date: 11/3/2024

Automatic bank services has not been performing well compared to the rest of my portfolio, so it is currently top of list for positions I may add to. The recent Q1 2025 results were slightly disappointing because of a slight drop in operating income from 38 million ILS to 36.8 million ILS, but this is a small quarterly dip, that is not representative of the long term pricing power that is entrenched within $SHVA.

Of course, there are still risks, like the company may not be able to raise prices due to regulation, and I could be wrong about the competitive environment in Israel.

You also get to collect a 3.49% yield while you wait for the thesis to materialize, and the company only trades for 12 times EV/EBIT.

Zengame Technologies $2660

Write up date: 6/5/2024

Zengame has been the biggest loser in the bunch here, due to a large drop in their ARPPU (average revenue per paying user). Despite this, their MAU (monthly active user count) has reversed directions now moving upwards.

This should be fine, as the consumer is being picky and less likely to spend, but the growth in MAU has shown that the consumer is staying within the Zengame ecosystem which is positive. Eventually the consumers wallets will follow the MAU, even if there is a delay, and the MAU is actually the most important metric.

Much of the thesis rests on their flagship game, Fingertip Mahjong, but they have a game called Fishing master that is climbing the ranks of the IOS top charts in China, plus some moonshot US games.

The low valuation protects from periods of lower profits, so investors can afford to wait and see how things shake out.

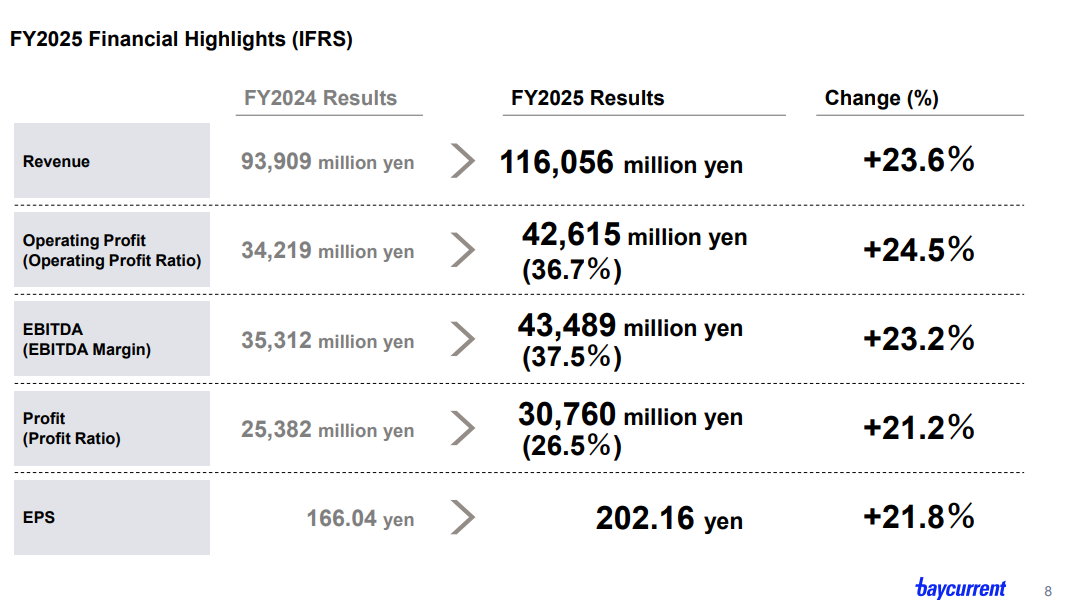

Baycurrent Consulting $6532

Write up date: 4/28/2024

Baycurrent has been my biggest winner by far, and I have taken some profits off the table, roughly a third of my original position sizing. The reason is that the P/E ratio is nearly 42 times the trailing twelve months.

Despite the high valuation, the company provides guidance for 20% growth every year, and I still don’t understand how it is possible to grow this much at their scale, but the company has been executing on this, and the stock price has reflected this.

I do not like consulting because it is a variable expense, and when times get tough it can be cut.

Additionally, the company understandably cut their buyback program for dividends because of the strong stock price.

I will likely hold a smaller portion of this stock because it is a great business with incredible management team.

The content in this newsletter is for informational and educational purposes only and does not constitute investment advice, financial advice, or a recommendation to buy or sell any securities. I may hold positions in the companies discussed.