A Quality Compounder from Japan

A Quality Compounder and a Deep Value Bet

I share my thoughts on a portfolio move to help myself become a clearer, more rational thinker. If you read this, please tell me how I can lose money. Thank you.

My first confession is that neither of the ideas are original and both come from Teddy Okuyama on X. My second confession is that I am new to Japanese securities, so you’ll have to excuse my ignorance. Despite this, I decided to take the jump to learn something new about Japanese culture, accounting, and common practices. The reason is If I’m not continuously learning, I will never be able to keep up in investing, a field that is ever changing.

The reason I became interested in these Japanese Securities is because if they were trading in the US they would be screaming buys from a quantitative standpoint. The reason I have not invested in Japan until this point is twofold. The first being the tendency for Japanese companies to hoard cash. I first observed this when I studied by employer’s financials (I’m employed by the US branch of a large-cap Japanese company). The business is incredible, but the cash hoard piles up with no sign of shareholder return. I have read that the reason for this is to pay the employees over shareholders in turbulent financial times. You can see why I’m happy to be an employee and not a shareholder. Secondly, the seeming decline in population created a good enough reason not to dig any deeper into potential investments.

BayCurrent Consulting 6532.T

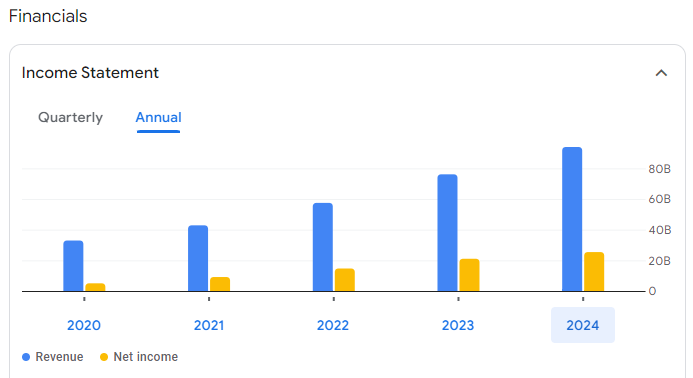

The first investment I decided to make is in what I believe to be a quality compounder trading at a fair to low valuation. The name is BayCurrent ($6532.T). It seems that those in Japan may know this as a household name. They are a consulting firm that focuses mostly on IT Services and Digital transformation. By the numbers, the operating record is stellar:

(JPY)

When I look at numbers like this I try and come up with explanations for why it happened this way. I try to understand what is the actual cause of such rapid growth in the addressable market. The consensus view is that the company has taken advantage of the “DX trend”. This means “digital transformation” which means preparing companies for the digital age.

The next step is the most important question: Can these stellar results continue? The first piece of evidence is the company medium term plan. They target 20% growth yoy. This is a lofty goal, after all, the market does not price in this growth. To me, the trend of digitalization is not slowing, but accelerating as it becomes ever important to integrate technology into business. Therefore, in order to keep up with the global economy, Japanese businesses must keep using firms like BayCurrent to stay relevant.

Secondly, what factors allow for a sustained market share? First understand that most of the competitors are global consulting giants such as: Deloitte, PwC, Accenture, and BCG.

Some believe that they are lower cost than alternatives because they are not weighed down by global headquarters. This also makes the business leaner and more apt to respond to changes in the domestic market. Additionally, there may be advantages to being a domestic company serving the domestic market.

Valuation

The Current expected yield from dividends is roughly 1.5% at the current price levels. The Current TTM PE is around 20. The EV/EBIT is roughly 13, which is very cheap from a historical standard.

At the current levels the FCF yield is around 4% per year. Over the long term, if the business continues to grow at an average rate of 15% per year, the valuation is very fair and investors can be rewarded.

Negative Sentiment

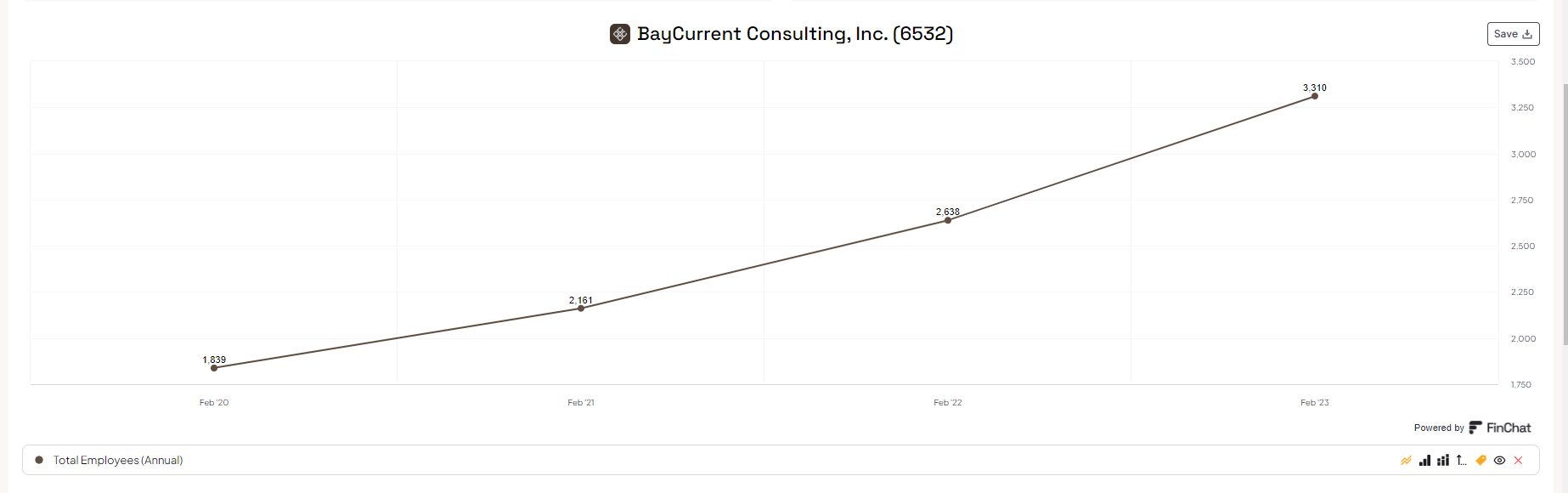

I’ve gathered that some of the negative sentiment behind the business is based on the labor pool. In 2024, Baycurrent’s workforce rose to 3,310 from 2,638 in 2023, many of which being less experienced consultants like new grads.

Source: Stratoshpere.io

Many have cited concerns with the quality of work coming from less experienced consultants. According to employee reviews on open work, it seems that the company operates on an “open pool” system. I believe this means the consultants can be swapped in an out of projects based on experience level required. This may be a system that efficiently allocates the tenured employees to the most impactful projects. Some have pointed out that this can also create a negative loop:

No Experience → Never get put on projects → Taken off projects → Never gain experience

This seems like a negative quality of the business, but consider the effects of this cycle. The quality of the consulting can never be brought down by new hires, until the culture has developed from newer employees to more experienced ones.

I will need to dig deeper to make a judgement, but I’m not concerned about the degradation of the business for a key reason. Even with the surplus of new hires to the company, company culture does not degrade overnight. The company was founded in 1998, even doubling the employee head count cannot reverse the long history and culture of the business.

Capital Allocation

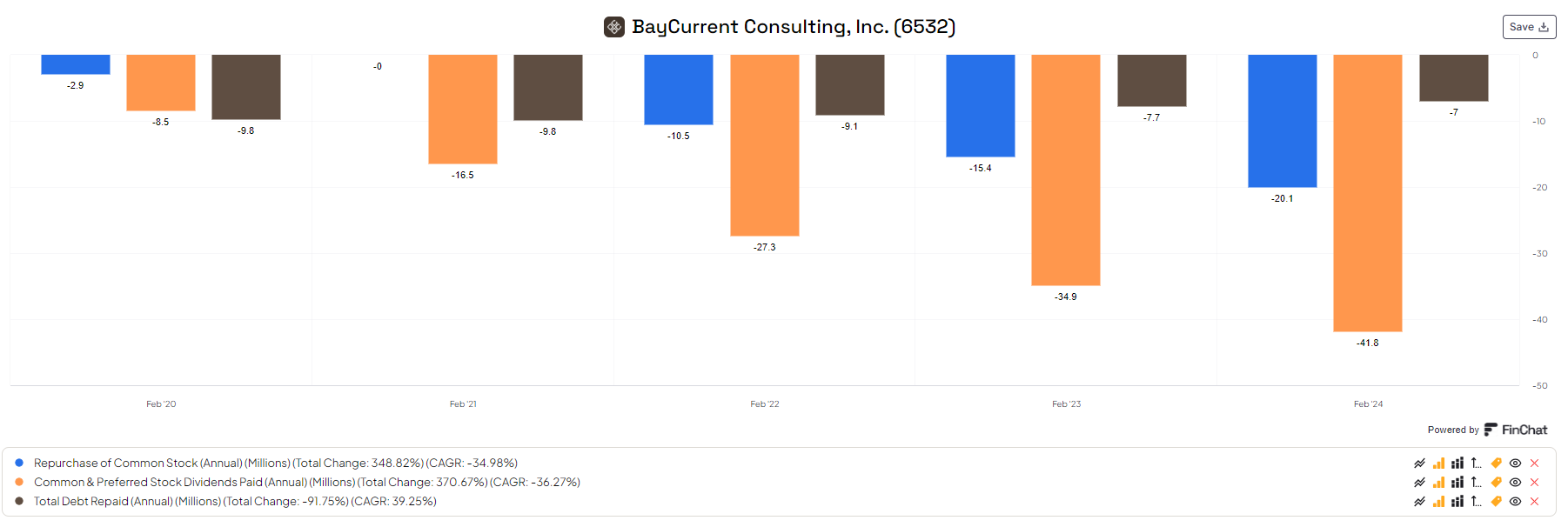

The reason I’m comfortable investing in this company is the management has agreed to pay out 40% of the earnings in a mix of dividends and buybacks. Of course, this does nothing to the cash that is already on the balance sheet doing nothing. Being that the company is shareholder focused enough to have a buyback program, I trust this capital will come to its rightful owners eventually. Even without shareholder returns from the balance sheet, history has shown that Japanese investors can enjoy great returns if the business performs well.

BayCurrents Financing Activities (Feb 20’ - Feb 24’) (Buybacks, Dividends, Debt repayment)

Population Decline

Whether population decline can impact the success of investing in Japanese securities is a complex issue. The ideal case when investing in Japan is choose a company that is tied to global wealth, like the second bet, so you don’t have to think through this issue at all.

But because Baycurrent’s customers are in the Japan ecosystem, we have to consider whether an aging population will affect future growth.

On the one hand, I do have concerns over dropping birth rates in Japan as with other developed nations like South Korea. On the other hand, productivity improvements from technology are likely to fuel GDP growth even in the face of an aging population. The equation for any modern economy is Productive hours X Productivity, and fewer working people means fewer productive hours. The other side of the scale, (productivity) is increased by technological improvements. Therefore, one can argue IT services and digital transformation consulting can be important and necessary in the wake of population decline. Finally, the main metric is that if real GDP growth continues at a fair pace in Japan, I am comfortable as an investor.

More to come on the second bet…

The content provided in this article is for informational purposes only and should not be construed as financial advice. The author is not a licensed financial advisor, and the information presented here does not constitute an offer or solicitation to buy or sell any securities.

Great pick. This played out well.